It keeps you stuck slowly—through systems designed to keep you paying, not progressing.

I remember when red was just a beautiful color.

A color people proudly wore.

A color of boldness, attraction, uniqueness. Red stood out. Red commanded attention.

People loved it. They still do.

But somehow, red has also become a silent horror in many lives.

Red has always signified danger. A warning sign. A “do not enter.” But today, millions of people are not just seeing red — they are living in it.

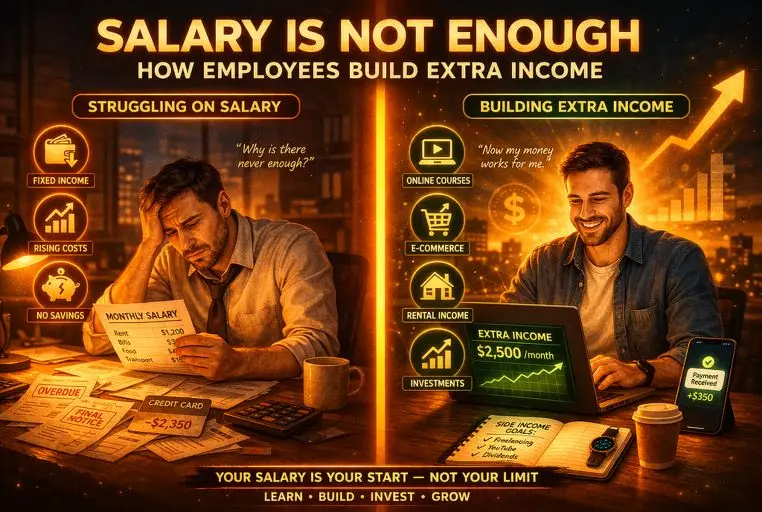

Not fashion red. But Financial red which mean debt

Many people wake up daily already behind. Bills waiting, loans due, credit alerts blinking and overdrafts stretched.

Salaries arriving only to disappear within hours.

They work all day at their primary job. Eight hours. Ten hours. Sometimes twelve. And when the day ends, instead of rest, they start another hustle: Ride-hailing, freelancing, online gigs, weekend shifts and so on.

More responsibility, little pay, less time for themselves and even less peace.

- They are exhausted but cannot stop.

- They are tired but cannot rest.

- They are earning but not progressing.

And here’s the deeper issue: the more tired they become, the less clarity they have.

When you are constantly in survival mode, you don’t think strategically. You think urgently.

Urgency keeps you moving. Strategy changes your position.

This is the life of many people. And if nothing changes intentionally, it will not magically get better.

Because so many things are happening so fast. Things like:

1. Inflation increasing.

2. Expenses expanding.

3. Responsibilities growing.

4. Energy declining.

Without a shift in direction, many will remain stuck. Not because they are lazy, but because they are trapped in a cycle of earning to repay, working to survive, borrowing to breathe.

Millions are walking around with heavy responsibilities and little support. Some are supporting parents. Some are raising children. Some are paying school fees for siblings. Some are trying to build something quietly.

They finish their primary job and start another just to keep up. And those who cannot take on extra work resort to borrowing. By the time salary arrives, most of it is already allocated to debt repayment. Sometimes even before payday, new debts have already formed.

It becomes a loop: Work, Borrow, Repay and Work again.

So The Question Becomes: How Do We Break This Red Cycle?

Before we answer that, let’s talk about something deeper.

Many people have had what I call “Peter’s experience.”

In the Bible, Peter fished all night and caught nothing. Imagine working hard for years and seeing little results. Imagine trying business, failing. Trying relationships, failing. Trying opportunities, failing.

It costs you time. It costs you pride. It costs you confidence.

At some point, you quit trying differently. You just follow trends. You take what comes. You stop believing something unique can work for you.

Even while struggling, you tell yourself, “At least I’m not trying that again. I don’t want that pain.”

Your past disappointments begin to control your future decisions.

But here’s the truth: quitting strategy is not the same as quitting effort.

Many people are working harder than ever, but they are no longer working strategically.

So How Do We Solve This?

There is only one sustainable way out of constant financial red.

Solve a problem.

That question sounds simple: What Problem Can You Solve?

But it is deeper than it looks.

This question forces you to shift from “How can I earn money?” to “How can I create value?”

When you focus only on earning, you compete with millions of people for limited jobs.

When you focus on solving, you create demand.

For example, someone might say, “I’m good at calculations.”

That sounds ordinary.

But if you say, “I help people who struggle with numbers to calculate faster and more accurately,” that becomes a solution.

You may not be a math teacher. You may not stand in a classroom. But you could create content that simplifies business calculations, budgeting formulas, profit margins, loan breakdowns, and daily financial planning.

Students, entrepreneurs, freelancers — different groups — will come because you are solving a real problem: confusion with numbers.

The issue with many people is that we box ourselves into titles instead of positioning ourselves around problems.

“I am a writer” focuses on what you are.

“I help businesses increase sales using persuasive words” focuses on what you solve.

People don’t pay for titles. They pay for solutions.

Saying “I build houses” sounds impressive.

But saying “I help people design affordable houses that match their income before they start building” speaks directly to someone’s fear and dream.

The house is the goal. The drawing is the beginning. If you can help at the beginning, you become trusted for the bigger stages.

When you focus on problems instead of titles, opportunities expand. Your burden begins to reduce because income becomes tied to value creation, not just time exchange.

Now, How Do You Discover The Problem You Can Solve?

First, observe your frustrations. What do you complain about often? Where do you see inefficiency? Sometimes the problem you can solve is hidden inside what irritates you daily.

Second, review your natural strengths. What do people ask you for help with repeatedly? Advice? Technical setup? Writing captions? Fixing phones? Budgeting?

Repeated requests reveal perceived value.

Third, examine your experience. What have you survived that others are currently struggling with? Debt recovery? Job searching? Learning a skill from scratch? Those experiences can become solutions.

Fourth, test small. Create content, offer small help, volunteer your skill in small communities. Notice where engagement increases. Attention is data.

Fifth, refine your positioning. Move from “I do X” to “I help Y achieve Z.” That clarity attracts the right audience.

Now, How Do You Sell What You Can Solve?

Selling is not shouting. Selling is clarifying.

First, define the pain clearly. If you help freelancers manage irregular income, speak directly to the fear of unstable cash flow.

Second, show proof. Share results. Share testimonials. Share your own transformation story.

Third, simplify your offer. Instead of offering ten random services, package one clear outcome. For example: “I help side hustlers create a simple weekly budgeting system that prevents debt.”

Fourth, price based on value, not insecurity. If your solution saves someone ₦200,000 in financial mistakes, charging ₦30,000 for guidance is reasonable.

Fifth, build trust consistently. Content, conversations, free insights — these build authority over time.

The red life — the debt cycle — reduces when income increases beyond survival. And income increases sustainably when value increases.

Conclusion

Red used to be a color of beauty.

Now, for many, it represents financial pressure.

But the way out is not endless hustle alone. It is not working 18 hours daily without direction.

The way out is clarity.

Clarity about the problem you can solve. Clarity about the value you can create. Clarity about positioning yourself beyond titles.

You may have tried before and failed. You may have cast your net and caught nothing.

But this time, don’t cast it randomly. Cast it with strategy. Cast it with value. Cast it with positioning.

When you move from earning to solving, from title to transformation, from survival to strategy — the red in your life can slowly begin to fade.

And in its place, stability begins to grow.

Final Word

If you are serious about growth — financial or personal — but tired of vague advice and repeated setbacks, you are in the right place.