I remember when I first sat down to design what looked like a perfect financial plan around a hire purchase agreement.

Everything looked reasonable.

- The numbers made sense.

- The monthly payment looked affordable.

- My income at that time could comfortably handle it.

On paper, the plan was strong.

But something interesting happens when financial plans move from the spreadsheet into real life.

Life is not as stable as numbers. Income changes. Businesses slow down. Emergencies appear. Priorities shift. Opportunities suddenly require cash you already committed somewhere else.

And that is when a different type of challenge begins to show up and not the financial math, but the financial pressure.

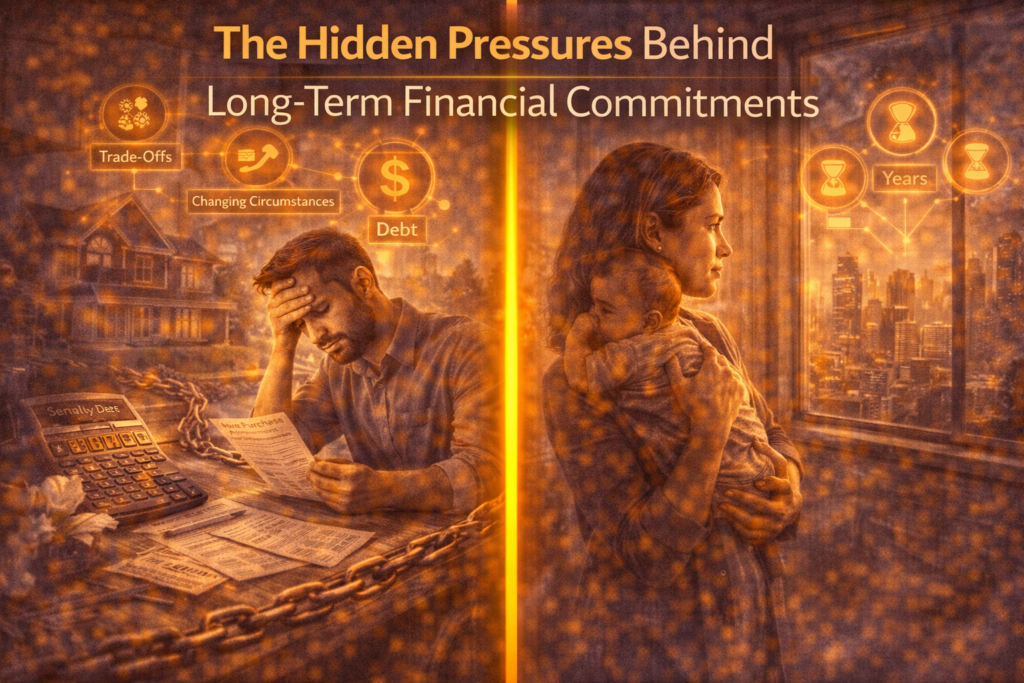

Hire purchase, installment plans, or long-term financial commitments are not only about whether you can afford the monthly payment today. The real challenge is whether you can sustain the commitment emotionally, financially, and psychologically over time.

For example, someone might take a car through hire purchase for ₦4.8 million and agree to pay ₦100,000 monthly for 48 months. At the beginning, the excitement is high. The monthly payment feels manageable. But four years is a long time.

Income may fluctuate. Unexpected expenses may appear. Personal priorities may change. What once felt like a comfortable financial decision can slowly become a mental burden if it was not carefully prepared for.

In a previous article, I explained how hire purchase works, the risks involved, and how to approach it with proper financial planning. That article lays the foundation for understanding the issues of hire purchase agreements and the mindset needed before signing one.

(You can read that foundation article here: Hire Purchase: Opportunity or Financial Trap?).

What we will focus on here is something deeper.

Even when someone understands hire purchase well and plans carefully, there are still psychological and financial pressures that can appear along the journey.

Understanding these pressures early can help you prepare for them instead of being surprised by them later.

1. Pressure of Income Consistency

What the new challenge is

One of the first pressures that appear during a long-term commitment is the fear that income may not remain stable.

You may design your repayment plan based on your current income. Everything looks safe. But months later, your financial environment may change.

- Business might slow down.

- A major client might delay payment.

- Your salary might arrive later than usual.

Suddenly, the question begins to appear in your mind: What if my income drops below what I planned for?

The commitment that once felt comfortable begins to create pressure.

Why it appears

Income is rarely perfectly consistent over long periods. Even stable jobs experience delays, restructures, or unexpected disruptions. Entrepreneurs and freelancers experience income fluctuations even more frequently.

When financial plans assume income will remain steady for years, any change can create stress.

The common mistake people make

Many people plan based only on what they can afford today.

If someone earns ₦300,000 monthly and agrees to pay ₦100,000, the math seems simple. But that payment already consumes one-third of their income. If anything unexpected happens, the margin becomes too tight.

People often underestimate how quickly financial pressure can appear when the gap between income and obligation is small.

How to prepare for it

Preparation means building financial buffers.

Instead of planning around the exact repayment amount, create capacity beyond it. If your obligation is ₦100,000 monthly, your finances should comfortably handle much more.

This is where the 2× capacity mindset becomes useful. It ensures that even if income weakens temporarily, repayment discipline can continue.

Saving extra funds alongside the monthly payment can also create emergency buffers that protect you during difficult months.

What to expect if handled well

When income volatility is anticipated, temporary setbacks become manageable.

Instead of panic, you simply rely on the financial cushion you prepared earlier.

2. Pressure of Over-Optimization

What the new challenge is

Another hidden pressure appears when someone tries too hard to manage their finances perfectly.

They begin monitoring every naira they spend. Every purchase becomes something to analyze. Even small expenses start feeling like threats to their financial plan.

Instead of feeling financially responsible, they begin to feel financially anxious.

This is the pressure of over-optimization.

Why it appears

When people take on long-term commitments, they naturally want to avoid failure. To stay in control, they tighten their financial habits.

They reduce spending. They calculate everything. They constantly track their accounts.

But excessive monitoring can slowly turn into mental stress.

Instead of money serving them, they start serving the financial system they created.

The common mistake people make

The mistake is turning financial awareness into financial obsession.

Some people become so focused on controlling every detail that they remove flexibility from their lives.

They forget that financial systems should support life not create constant psychological tension.

How to prepare for it

A healthier approach is building structured flexibility into your financial plan.

Budgets should include reasonable room for lifestyle spending and unexpected small expenses. Financial discipline should exist, but it should not require constant emotional attention.

Good financial systems work quietly in the background.

What to expect if handled well

When financial planning balances discipline with flexibility, the system becomes sustainable.

You stay responsible with money while still enjoying financial peace of mind.

3. Pressure of Early Repayment Regret

What the new challenge is

Many people feel motivated to eliminate debt as quickly as possible. So when they begin earning extra income, they rush to push large amounts toward early repayment.

At first, this feels smart. But later, situations may arise where cash becomes important.

- A business opportunity appears.

- An emergency expense arises.

- Income temporarily slows down.

Then regret appears. Maybe I should not have rushed to clear the balance so quickly.

Why it appears

Debt repayment gives psychological satisfaction. Clearing obligations early feels like financial victory.

However, focusing entirely on repayment can reduce liquidity.

Without accessible cash reserves, even small financial disruptions can become stressful.

The common mistake people make

The mistake is prioritizing debt elimination while ignoring cash flow flexibility.

Some people direct every extra naira toward repayment and leave themselves with little financial cushion.

When unexpected needs appear, they realize they sacrificed liquidity too early.

How to prepare for it

A balanced approach works best.

Continue reducing debt gradually, but also maintain savings and emergency funds. Liquidity gives you the ability to handle unexpected situations and seize opportunities.

Debt reduction should not destroy financial flexibility.

What to expect if handled well

When repayment and liquidity are balanced, financial progress becomes stable. You reduce obligations while still maintaining the ability to respond to new opportunities or financial shocks.

4. Pressure of Long-Term Commitment Fatigue

What the new challenge is

One pressure many people underestimate is emotional fatigue from long commitments.

A 48-month installment plan means committing to something for four years.

At the beginning, motivation is strong. The purchase feels exciting. The financial plan feels strategic. But human motivation changes.

By the third year, the same commitment may begin to feel restrictive.

Why it appears

Life evolves.

Your career may change. Your priorities may shift. Your financial goals may grow. Something that once felt necessary might no longer feel important.

But the payment obligation remains fixed.

This emotional mismatch creates commitment fatigue.

The common mistake people make

Most people focus only on whether they can afford the payment today.

They rarely ask whether they will still feel comfortable with the commitment several years later.

Financial agreements last longer than emotional excitement.

How to prepare for it

Before entering long commitments, consider your long-term direction.

Ask whether the asset truly supports your future goals or if it is simply solving a short-term desire.

Financial commitments that align with productivity or long-term growth are easier to sustain than those driven by temporary excitement.

What to expect if handled well

When commitments are aligned with long-term value, emotional fatigue reduces.

Instead of feeling trapped by the obligation, the commitment becomes part of your larger financial journey.

Conclusion

Most people assume financial commitments fail because of numbers.

But in reality, they often fail because of pressure.

Hire purchase and installment systems are not inherently bad. They have helped many people access opportunities faster than their savings would allow.

But these systems require preparation.

When someone enters a long-term commitment with financial buffers, clear contract terms, and a productive purpose, the journey becomes manageable.

Without preparation, even a mathematically sound plan can become emotionally exhausting.

And that is why understanding the structure of hire purchase and the pressures that follow it is important before signing any agreement.

Final Word

If you are serious about growth — financial or personal — but tired of vague advice and repeated setbacks, you are in the right place.